As an SEO expert, I’ve learned that timing is everything. Whether you’re trying to rank a new blog post or time the housing market, you need to understand the underlying “algorithm” driving the trends. Right now, the most searched question in the real estate world is: are mortgage rates expected to go down?

After a volatile 2025 that saw rates touch nearly 7% before cooling off, 2026 has brought a mix of cautious optimism and fresh geopolitical challenges. As of April 18, 2026, the average 30-year fixed rate sits at 6.34%. While this is significantly lower than the peaks of two years ago, it is still far from the “3% dreams” of the pandemic era.

In this comprehensive 2026 update, we will analyze the data from the Federal Reserve, the bond market, and leading economists to answer whether are mortgage rates expected to go down and how you should plan your next move.

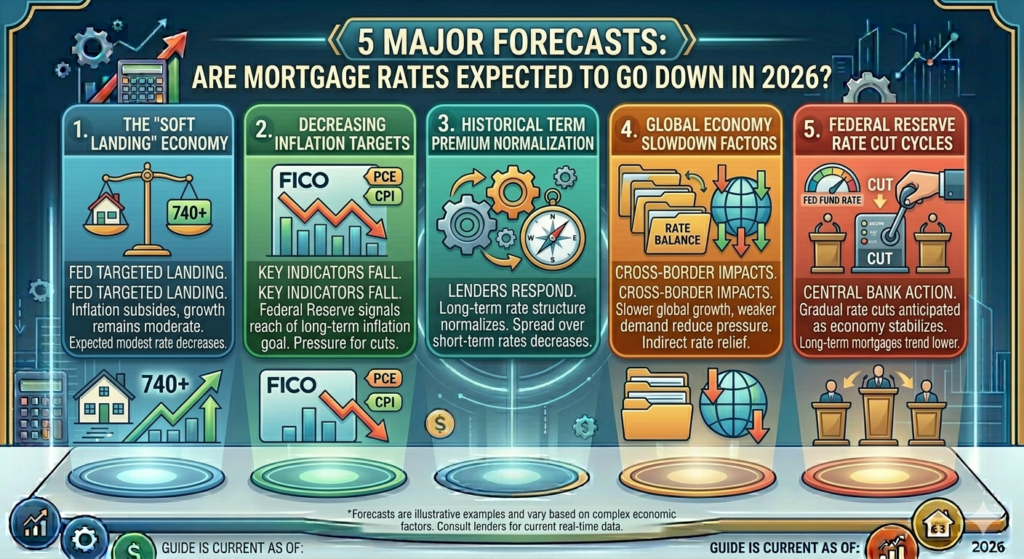

1. The 2026 Reality: A Thaw, Not a Flood

The short answer to the question are mortgage rates expected to go down is: yes, but with a “side of volatility.” Early in 2026, rates hit a yearly low of 6.09%, sparking a wave of buyer activity. However, recent energy price shocks and international tensions have pushed them back up toward the 6.4% range.

Economists at Morgan Stanley and Fannie Mae suggest that the overall trajectory for the next 18 months remains downward. The goal for many analysts is a stabilization point between 5.50% and 5.75% by mid-2026, assuming inflation continues its slow descent toward the 2% target.

2026-2027 Mortgage Rate Forecast (Table)

| Expert Source | 2026 Year-End Prediction | 2027 Forecast | Sentiment |

|---|---|---|---|

| Morgan Stanley | 5.75% | 6.00% (Slight Rise) | Optimistic |

| Fannie Mae | 6.00% | 5.90% | Stable |

| MBA | 6.40% | 6.40% | Cautious |

| NAHB | 6.14% | 6.01% | Improving |

Export to Sheets

2. Why the Federal Reserve is “Staying Patient”

If you want to know are mortgage rates expected to go down, you have to watch the Federal Reserve’s “dot plot.” In their recent April 2026 communications, Chair Jerome Powell described the current monetary policy as “mildly restrictive.”

The market had originally anticipated two or three rate cuts in 2026. However, due to recent oil price spikes, the consensus has shifted toward one single 25-basis-point cut later this year. When the Fed eventually cuts their benchmark rate, it lowers the cost for banks to lend, which is a primary reason why are mortgage rates expected to go down in the long-term forecast.

3. The 10-Year Treasury Yield: The “Leading Indicator”

In SEO terms, the 10-year Treasury yield is the “Search Console” of the mortgage world. It shows you the truth before the headlines do. Mortgage rates are closely tied to these yields.

In mid-2025, the yield fell toward 3.75%, which allowed mortgage rates to drop. Currently, in April 2026, the yield is fluctuating due to “flight to quality” investors reacting to global conflicts. For are mortgage rates expected to go down to become a reality, we need to see the 10-year yield stabilize and stay below 4%.

4. The “Lock-In Effect” is Finally Breaking

One of the biggest hurdles in the 2024-2025 market was the “lock-in effect”—homeowners with 3% rates refusing to sell. This kept inventory low and prices high.

As the answer to are mortgage rates expected to go down shifted toward the low 6% range, the math started to change. We have seen a 12% increase in new listings this spring. Homeowners are realizing that waiting for 3% is a losing game, and 6% is the “new normal” they can live with. This increase in supply is crucial because it prevents home prices from skyrocketing even as rates dip.

5. Inflation: The Ultimate “Algorithm” Update

Inflation is the most important factor determining are mortgage rates expected to go down. As of the latest February 2026 reports, headline inflation has cooled significantly.

- Core Inflation: Currently around 2.3%.

- Target: 2.0%.

Because we are so close to the target, the pressure on the Fed to keep rates high is easing. However, the recent “energy shock” in early 2026 is a wildcard. If gas prices stay high, inflation could tick back up, which would mean the answer to are mortgage rates expected to go down might be “not yet.”

6. Comparing Loan Types in Today’s Market

Even if the national average is 6.34%, the answer to are mortgage rates expected to go down for you depends on the product you choose.

Current Rates by Product – April 18, 2026 (Table)

| Loan Type | Current Rate | Weekly Change | Best For |

|---|---|---|---|

| 30-Year Fixed | 6.34% | -0.06% | Long-term stability |

| 15-Year Fixed | 5.72% | -0.08% | Rapid equity growth |

| FHA 30-Year | 5.96% | Stable | Low down payment |

| VA 30-Year | 6.24% | Stable | Veterans & Military |

| 5/1 ARM | 5.68% | -0.02% | Short-term buyers |

Export to Sheets

7. The Strategy: “Marry the House, Date the Rate”

As an SEO specialist, I often recommend “testing and iterating.” The same applies here. If you find a home that fits your life but you’re worried about whether are mortgage rates expected to go down, remember that you aren’t stuck forever.

Many 2026 buyers are choosing to buy now—avoiding the massive bidding wars that will inevitably happen if rates hit 5.5%—and planning to refinance in 2027. If are mortgage rates expected to go down further next year, you can simply “update” your loan.

8. Regional Impact: Where Are Rates Falling Fastest?

While national numbers are helpful, real estate is local. In “tech hubs” where the economy is cooling slightly, lenders are becoming more aggressive to win business.

In the South and Midwest, we are seeing “rate buydowns” become a standard part of the negotiation. If you ask a builder or seller to pay for a 2-1 buydown, your effective rate for the first year could be 4.34%, even if the current market answer to are mortgage rates expected to go down is stuck at 6%.

9. The 2027 Outlook: A Return to 5%?

Looking further ahead, the answer to are mortgage rates expected to go down becomes even more interesting. The National Association of Home Builders (NAHB) predicts that by 2027, the 30-year average will fall to 6.01%.

Some aggressive forecasts suggest that if a recession hits in late 2026, we could see a brief dip into the high 4% range. However, most experts agree that the structural changes in the global economy make the “sub-4%” era a thing of the past.

10. Summary Table: The “Why” Behind the Moves

| Factor | Current Impact | Future Prediction |

|---|---|---|

| The Fed | Pausing / Restricted | One cut late 2026 |

| Oil Prices | High (Inflationary) | Likely to stabilize |

| Housing Supply | Increasing (+12%) | Balanced by 2027 |

| Buyer Demand | Moderate | High (if rates hit 5.8%) |

Export to Sheets

Frequently Asked Questions (FAQs)

Are mortgage rates expected to go down below 5% in 2026?

Most major institutions, including Fannie Mae and the MBA, do not expect rates to drop below 5% in 2026. A more realistic “floor” for this year is the 5.75% to 6.0% range.

How does the Iran conflict affect mortgage rates?

Geopolitical conflicts often drive up oil prices. Since higher energy costs lead to higher inflation, these conflicts can actually prevent rates from falling as fast as originally predicted.

Should I wait for rates to drop before I buy?

Waiting can be risky. If the answer to are mortgage rates expected to go down is a drop to 5.5%, thousands of buyers will jump back into the market, which could drive home prices up by more than the amount you save on interest.

When will the next Fed rate cut happen?

Market odds currently favor a rate cut in the final quarter of 2026, though this is subject to change based on upcoming inflation and employment data.

Can I refinance if I buy at 6.34% today?

Yes. If are mortgage rates expected to go down to 5.5% in 2027, most experts suggest you wait until there is at least a 0.75% to 1% difference in rates before refinancing to cover the closing costs.

What is the current “variability” in the market?

The Mortgage Rate Variability Index is currently a 7 out of 10. This means there is a wide range of offers between different lenders. You should shop around to find which bank’s version of are mortgage rates expected to go down benefits your specific credit profile.

Conclusion

The evidence suggests that we are in a long-term “cooling” phase for interest rates. While the question are mortgage rates expected to go down is met with a “yes,” it’s important to realize that the descent will be slow and full of minor peaks and valleys.

As we move through the rest of 2026, stay focused on the data. Monitor the 10-year Treasury yield, watch the Fed’s signals on inflation, and keep an eye on your local inventory levels. Just like SEO, the housing market rewards those who are patient, data-driven, and ready to pivot when the “algorithm” changes in their favor.

Whether you decide to buy today or wait for the 5.75% mark, knowing are mortgage rates expected to go down gives you the strategic advantage you need to secure your financial future.

Disclaimer: Real estate and mortgage trends are based on current market projections as of April 18, 2026. Financial decisions should be made in consultation with a licensed mortgage professional.